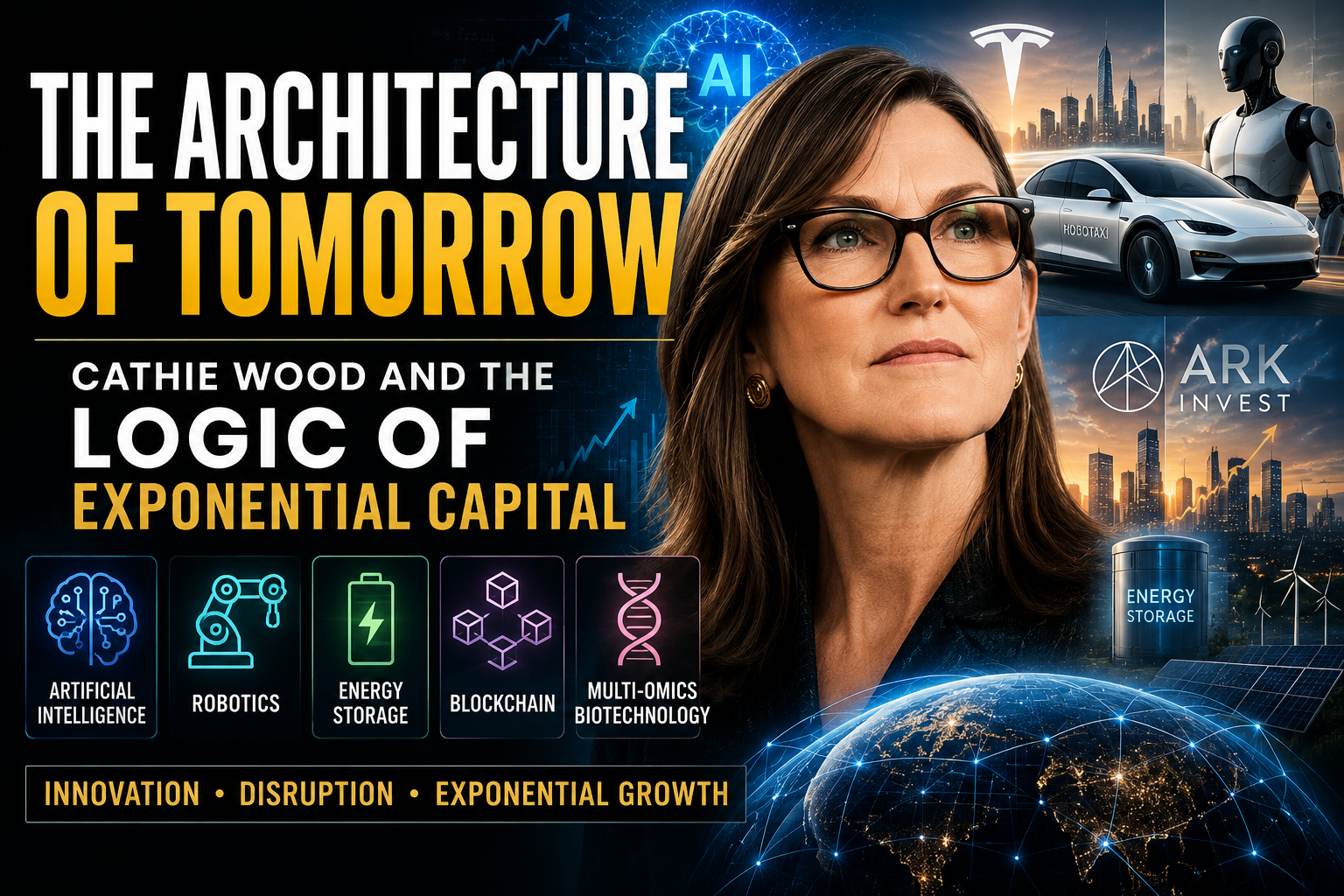

Cathie Wood and the architecture of exponential capital, featuring AI, robotics, Tesla, blockchain, biotechnology, and future economic networks

Introduction

Cathie Wood does not belong to the tradition of financial commentary. She belongs, more accurately, to the tradition of civilizational argument—the kind practiced by those who believe that the allocation of capital is, at its root, a philosophical act. When she appeared on Steven Bartlett’s The Diary of a CEO, she did not speak like a fund manager defending a thesis under pressure. She spoke like someone who had already resolved the most important intellectual questions and was now simply waiting for the rest of the world to catch up. That posture — patient, exact, and entirely uninterested in conventional validation — is itself a statement about the era we inhabit.

What distinguishes Wood from the broad class of technology optimists is not the boldness of her projections but the structural coherence underlying them. Most futurists operate by extrapolation: they identify a trend, extend it forward, and declare the outcome inevitable. Wood operates differently. Her framework is built on the interdependence of innovations — the idea that artificial intelligence, robotics, energy storage, blockchain, and multi-omics biotechnology are not parallel developments but interlocking ones, each accelerating the others in ways that produce not additive but multiplicative outcomes. This is a harder intellectual position to hold, and a harder one to defend, but it is also a more honest description of how technological revolutions actually work.

The podcast itself — a long-form conversation between a practitioner of speculative capital and a practitioner of popular intellectual discourse — created an unusual space for Wood to articulate what ARK Invest’s research reports, for all their empirical density, rarely achieve: a unified philosophical account of what innovation means. Bartlett’s questions, at their best, pushed Wood toward first principles rather than market commentary. The result is one of the more important public documents about investment epistemology produced in recent years, not because of any single prediction Wood makes, but because of the reasoning architecture she exposes beneath those predictions.

Understanding that architecture requires recognizing that Wood is making two separate but related claims. The first is empirical: that five specific technological platforms are converging in ways that will generate unprecedented economic value over the next decade. The second is normative: that investors who fail to orient themselves toward this convergence are not simply making a strategic error but are also, in a meaningful sense, failing to understand the moment they are living through. These claims reinforce each other, but they should be assessed independently. The empirical claim can be evaluated against data; the normative claim requires a different kind of engagement.

It is also worth situating Wood within the intellectual history of disruptive investment theory. The lineage here runs through Clayton Christensen’s work on disruptive innovation, through the venture capital frameworks developed in Silicon Valley across the 1990s and 2000s, and back further to Schumpeter’s concept of creative destruction. Wood stands in this tradition but pushes beyond it in one important respect: she argues that the current wave of disruption is not industry-specific but civilizational. It will not replace one sector’s incumbents with new entrants while leaving the broader economic structure intact. It will restructure the economic structure itself — the relationship between labor and capital, between physical and intellectual assets, between national and post-national economic organization.

For the global expert community — economists, technologists, policy architects, and institutional investors — Wood’s argument poses a direct challenge. Mainstream macroeconomics still largely models the economy using frameworks built for industrial-era production functions. The assumption that productivity grows smoothly, that capital and labor combine in stable ratios, that technological change is an external shock rather than an endogenous driver — these are not just theoretical conventions. They shape how institutions allocate resources, how governments design tax regimes, and how portfolio managers construct risk models. Wood’s thesis, if taken seriously, implies that most of these frameworks are not merely incomplete but actively misleading.

This essay engages with Wood’s thinking at the level of its deepest premises. It is not a summary of her investment positions; those are available elsewhere and shift as market conditions evolve. It is an attempt to reconstruct the intellectual logic that underlies those positions — to examine what Wood actually believes about technological change, economic organization, and the moral dimensions of capital allocation, and to assess where that logic holds and where it requires qualification. The argument is presented across nine sections, each corresponding to a dimension of Wood’s framework, and each attempting to carry the analysis further than the original conversation alone permits.

The stakes of this engagement are not academic. If Wood’s convergence thesis is substantially correct, then the next decade will see a reallocation of global capital at a scale not witnessed since the electrification of industrial economies in the early twentieth century. The institutions, nations, and individuals that understand the logic of that reallocation will participate in the creation of enormous value. Those that do not will experience, to varying degrees, the consequences of structural irrelevance. Few intellectual questions are more practically consequential, and few are more poorly served by the quality of public debate currently surrounding them.

Disruptive Vision and The Big Shift

When Bartlett asked Wood to identify the best investment for building wealth in the future, he was posing what seemed like a tactical question. Wood converted it into a strategic one — and then into a philosophical one. Her response did not begin with an asset class or a ticker symbol. It began with a claim about the nature of the current moment: that we are living through a structural break in economic history, not a cyclical fluctuation within a stable system. This move, from the tactical to the civilizational, is characteristic of her thinking and is the right move — because no portfolio strategy makes sense outside of an accurate account of the environment in which it will operate.

The concept Wood deploys to describe this moment — “The Big Shift” — is not original to her. Variants of it appear across decades of technology commentary. What Wood does with it that is intellectually distinctive is insist on its specifically exponential character. She is not claiming that things are changing faster than usual. She is claiming that the rate of change is itself accelerating—that the curve describing technological capability has bent sharply upward, and that this bending is not a phase transition after which things stabilize but a permanent property of the technological environment going forward. The difference matters because it determines whether conventional forecasting methods are valid. If change is merely rapid but linear, you can adjust your models. If it is exponential, you need an entirely different model.

This is why Wood is so dismissive of the investment logic that prevails in conventional institutional finance. When she criticizes analysts who evaluate disruptive companies using discounted cash flow models, or who compare AI-era companies against the earnings multiples of industrial-era firms, she is not making a stylistic objection. She is pointing out a category error — applying a tool designed for one environment to a fundamentally different one. A DCF model built on five-year earnings projections cannot capture the value of a company whose competitive moat consists of a data flywheel that doubles in density every eighteen months. The model isn’t wrong in the way an estimate can be; it’s wrong in the way a thermometer is for measuring voltage.

Wood’s treatment of artificial intelligence as the “axis” of this transformation — her phrase—reflects a precise understanding of what is different about AI relative to previous general-purpose technologies. The steam engine and electrification extended human physical capacity. The internet extended human communication capacity. AI extends human cognitive capacity — the capacity to process information, recognize patterns, and make decisions. This is a qualitative expansion in what machines can do for and alongside humans, and it sits at a different level of the economic production function than previous technologies. When cognition becomes partially automatable, the boundaries of what is economically possible shift in ways that affect every sector simultaneously.

The case of Apple illustrates how Wood applies this framework. Apple is, by most measures, an extraordinarily successful company — one of the most profitable in history, with brand loyalty that has endured decades of competitive pressure. And yet Wood suggests that even Apple is vulnerable to the current wave of disruption. The reason is not that Apple lacks talent or capital. It is that Apple’s architecture — hardware-driven, ecosystem-locked, with software as a complement to devices — may not be the right architecture for an AI-native economy. Companies that dominate one technological era often fail to dominate the next, not because they made strategic errors but because their identities were formed around a set of assumptions that the new era invalidates.

Tesla’s role in Wood’s framework is to serve as the existence proof of her thesis — the demonstration that a company organized around AI-native principles, rather than hardware-native or software-native principles, can generate value at a scale that conventional analysis systematically underestimates. She consistently argues that Tesla’s valuation must be understood in terms of the data network it is building — the billions of miles of real-world driving data that train its neural networks — rather than in terms of its vehicle manufacturing margins. This is not promotional rhetoric. It reflects a genuine theoretical position about where value resides in AI-era companies: not in physical assets but in proprietary learning systems that improve automatically as they scale.

The philosophical dimension of Wood’s vision — and she insists on this dimension — is that innovation is not merely an economic mechanism but a moral one. This claim is easy to dismiss as the kind of uplift language that fund managers deploy for marketing purposes. But Wood means something more specific by it. She argues that each major wave of technological innovation has expanded the scope of what human life can be — has reduced the fraction of human time consumed by drudgery, increased access to information and medicine, and broadened the range of choices available to ordinary people. AI, in her account, will do this again at a greater speed than any previous wave. Investing in this process is therefore not merely profitable but virtuous — an act of alignment with the direction of human development.

The Big Shift, as Wood frames it, ultimately requires not just a new investment thesis but a new epistemic posture. Investors, policymakers, and intellectuals formed by the assumptions of the industrial era are not simply missing opportunities when they fail to engage with AI-driven disruption; they are operating with a fundamentally incorrect model of how value is created and destroyed. The shift Wood is describing is as much about which questions to ask as about which answers to give. The ability to see the current moment accurately — to understand that exponential change cannot be assessed with linear tools — is itself the scarcest resource in the economy of ideas. And it is, paradoxically, available to everyone willing to abandon the comfort of frameworks that no longer fit.

Five Pillars of Innovation and Their Convergence Logic

ARK Invest’s five-platform thesis — artificial intelligence, robotics, energy storage, blockchain, and multi-omics biotechnology — is frequently presented in financial media as a list of growth sectors. This framing misses the intellectual point entirely. Wood is not arguing that five sectors will grow; she is arguing that five specific classes of technology have achieved a degree of maturity that makes their convergence both possible and, under competitive pressure, inevitable. The thesis is about interaction effects, not individual trajectories. Remove one pillar and the others are diminished; combine all five and the result is a self-reinforcing system capable of compressing decades of economic development into years.

Artificial intelligence serves as the connective tissue of the entire framework. This is not merely because AI is the most visible and commercially active of the five platforms at present, but because it is the only one that directly enhances the performance of the others. AI makes robots more adaptive, makes energy storage systems more efficient through better demand prediction, makes blockchain systems more useful through intelligent contract execution, and makes multi-omics research tractable by processing biological datasets that no human team could analyze unaided. Wood’s concept of AI as the “new axis” of the economy is not a figure of speech — it describes a functional dependency structure in which AI’s progress propagates through every other domain.

In Wood’s treatment, robotics is best understood as AI’s physical instantiation. The robotic systems that matter in her framework are not the fixed-program industrial robots that have populated manufacturing floors since the 1960s; they are adaptive systems capable of learning from their environment, generalizing across tasks, and operating in contexts that were not explicitly programmed. The economic implications of this distinction are enormous. Fixed-program robots are capital equipment: they increase productivity within a defined task but cannot respond to changing requirements. Adaptive robots, by contrast, can be redeployed across tasks and environments, so their economic value is not limited to any single application. When Wood speaks of companies that operate “without humans,” she is pointing toward a future in which adaptive robotics make certain production functions effectively fully automatable — not because every job disappears but because the marginal cost of adding robotic capacity approaches zero.

Energy storage is the most underappreciated of the five pillars precisely because it appears unglamorous relative to AI and biotechnology. But Wood’s insistence on its centrality is analytically sound. The electrification of transportation, the decentralization of power generation, and the full deployment of renewable energy all depend on advances in energy storage that enable using energy when and where it is needed, rather than only when and where it is generated. Without storage, solar and wind generation are structurally limited by their intermittency; with it, they become the cheapest and most scalable form of energy production in history. Wood sees the battery not as a product category but as an enabling infrastructure — the equivalent of the transmission line in an earlier era of electrification, without which all upstream investments in generation are underutilized.

Blockchain technology is the most intellectually contested of the five pillars, partly because it has attracted both genuine innovation and considerable charlatanism. Wood’s defense of its inclusion is that blockchain solves a specific and real problem that no prior technology has solved: how to establish verifiable trust in digital transactions without relying on a centralized intermediary. The importance of this is difficult to overstate for anyone who has thought seriously about the economics of institutional trust. Centralized intermediaries — banks, clearinghouses, title registries, certification authorities — impose costs on every transaction they underwrite, create single points of failure and corruption, and systematically disadvantage those who lack access to established institutions. Blockchain offers an alternative architecture that is, in principle, available to any party with internet access. Whether that principle has been fully realized in current implementations is a separate and largely answered question — no — but the principle itself is sound.

Multi-omics biotechnology is the pillar that most visibly illustrates Wood’s convergence thesis. Multi-omics refers to the simultaneous analysis of multiple layers of biological information — genomics, transcriptomics, proteomics, and metabolomics — to reveal how genes are expressed, how proteins fold, and how metabolic pathways interact across an organism’s full biological complexity. This was computationally intractable until AI-based analysis tools made it possible to process the relevant datasets in reasonable timeframes. The result is a new era of biology in which the mechanisms of disease can be understood at a level of precision that makes genuinely predictive medicine feasible — not medicine that identifies risk factors probabilistically but medicine that can predict, years in advance, which specific diseases a particular individual will develop and intervene before symptoms appear. Wood’s phrase “AI for the human body” is accurate: the relationship between AI and multi-omics is structural, not peripheral.

The convergence among these five pillars is not hypothetical future speculation; it is already partially underway. Electric vehicles combine AI, energy storage, and adaptive robotics in a single platform. Genomic medicine combines AI and multi-omics. Decentralized finance combines blockchain and AI-based risk assessment. Each convergence creates a new domain of value that did not exist before and that cannot be adequately understood by analyzing either constituent platform in isolation. This is the core of Wood’s investment philosophy: value in the current era resides disproportionately at the intersections, not in the platforms themselves. Companies that occupy a single platform will experience growth; companies that integrate multiple platforms will experience transformative expansion.

The investment logic that follows from this convergence thesis is not obvious and is frequently misapplied even by those who nominally accept Wood’s framework. If five platforms are converging, the correct portfolio strategy is not to identify the best company in each platform and hold five positions. It is to identify companies that are actively integrating multiple platforms — that are building at the intersections — and to overweight them relative to single-platform players. This is a harder analytical task because convergence companies are often misclassified: Tesla is classified as an automobile manufacturer, and Palantir as a defense contractor. Neither classification captures what these companies actually are. The ability to see through industrial-era classification systems into the underlying technological architecture is, for Wood, a core competency of serious investment analysis in the current period.

Tesla, Robotaxi, and the Autonomous Economy

The dominant analytical failure surrounding Tesla in the investment community is a category failure. When analysts evaluate Tesla against automotive peers — Toyota, Volkswagen, General Motors — they are making a category error that produces systematically incorrect valuations in both directions. When Tesla’s stock was at levels that made this comparison look absurd in one direction, the bears were right to be skeptical. When it trades at multiples that the automotive comparison cannot justify, the bulls are right to insist that the comparison is wrong. What neither camp has fully worked out is what the correct comparison is — which requires first working out what Tesla actually is.

Wood’s answer is that Tesla is a real-time AI training system that happens to generate cash flow from vehicle sales. This is not a clever reframing designed to justify an aggressive price target. It is a structural description of how Tesla’s competitive position is built and maintained. Every Tesla vehicle on the road is a data-collection node in a network that continuously and at scale feeds training data to Tesla’s neural network systems. By mid-2024, Tesla had accumulated more than a billion miles of real-world driving data — data recorded in the messiest, most unpredictable conditions that autonomous systems will encounter. This dataset is a competitive moat in the exact technical sense: it would cost a competitor not just money but time — years of real-world operation — to replicate it. Unlike a patent, it cannot be licensed or reverse-engineered. Unlike brand loyalty, it cannot be eroded by better marketing. It is structural.

The neural network architecture that Tesla is building atop this dataset is designed to do something that rules-based autonomous driving systems cannot: generalize. Rules-based systems — the approach pursued by many early autonomous vehicle programs — encode explicit instructions for specific scenarios. They perform well in conditions that closely resemble their training environment and fail unpredictably in novel situations. Neural networks trained on sufficiently diverse real-world data develop implicit representations of driving that generalize across novel scenarios in ways that approximate, and in specific measurable dimensions, exceed human performance. Tesla’s data advantage matters because it accelerates this generalization — because the neural network learns not just from the average driving scenario but from the full distribution of scenarios, including the rare and dangerous ones.

The robotaxi model that Wood describes — vehicles operating autonomously for hire, at a cost approaching $0.25 per mile — represents the economic endpoint of this technological trajectory. At that price point, the economic case for personal vehicle ownership collapses for most urban and suburban users. The total cost of personal vehicle ownership in the United States, including purchase, insurance, maintenance, fuel, and parking, averages between $0.60 and $0.80 per mile of actual use. A robotaxi service at $0.25 per mile, available on demand with no search or waiting friction, is cheaper, more convenient, and eliminates the cognitive burden of driving. The economic pressure this creates on the personal vehicle market is not gradual — it is the kind of discrete threshold effect that characterizes platform transitions.

The business model implications extend well beyond the vehicle market. Tesla’s robotaxi network, if it achieves the scale Wood projects, becomes a platform in the full economic sense: a two-sided marketplace that connects riders and fleet capacity, governed by algorithms that optimize utilization, routing, and pricing in real time. The value of this platform is not proportional to the number of vehicles; it scales with the network density relative to demand density in specific geographies. This means that once a robotaxi network achieves critical density in a given market, its unit economics improve while competitors’ remain constant — the classic dynamic of network-effects businesses, now applied to physical transportation infrastructure.

Wood also addresses the implications of widespread robotaxi adoption for urban transformation with greater seriousness than most analysts. If autonomous vehicles become the dominant mode of urban transportation, the physical geography of cities changes. Parking — which currently consumes between 15 and 30 percent of urban land area in American cities — becomes redundant infrastructure. The economics of retail and commercial real estate, which currently depend heavily on parking accessibility, shift accordingly. The concentration of vehicle traffic at certain hours, which currently determines road capacity requirements, flattens as algorithmically coordinated fleets distribute trips more efficiently over time. These are not second-order effects; they are first-order economic and political consequences that will require active policy responses.

The social implications Wood raises are equally important and less frequently engaged. If vehicles generate income for their owners when not in personal use, the economics of vehicle ownership shift: a Tesla becomes more like a dividend-paying asset than a depreciating consumer good. This changes the income distribution effects of vehicle ownership in complex ways. On one hand, it creates a new income stream for those who can afford a Tesla. On the other hand, it may accelerate the concentration of this benefit among those with capital to invest in fleet assets rather than distributing it broadly. Wood acknowledges this without fully resolving it — which is intellectually honest because the resolution will depend on regulatory choices that have not yet been made.

The deepest implication of Wood’s Tesla thesis is that the most important companies of the next two decades will be categorically different from those of the last two. The latter were mostly platform companies that organized information, search, social media, and e-commerce. The former will be platform companies that organize physical activity—transportation, manufacturing, healthcare delivery, energy distribution. The distinction matters because physical platforms have different competitive dynamics, different regulatory exposure, and different social consequences than information platforms. The regulatory battles of the 2010s over information platforms were consequential but relatively contained. The regulatory battles over physical AI platforms — autonomous vehicles, robotic manufacturing, AI-guided healthcare — will engage more directly with life, safety, and the fundamental organization of economic life. Tesla is the first major company to enter this territory at scale, which is why Wood treats its success as carrying implications far beyond its own balance sheet.

Investment Strategy in the AI Era

The central diagnostic that Wood applies to conventional investment practice is precise and damning: most institutional investors are trying to assess the future using instruments calibrated to the past. This is not carelessness or incompetence; it is the inevitable result of an industry whose standard of care is defined by peer comparison. A portfolio manager who deviates significantly from benchmark holdings faces career risk if the deviation produces underperformance, even temporarily. This creates a structural incentive to hold positions that can be defended by reference to consensus, which means, in practice, positions in companies whose value is legible through conventional analytical tools. Companies whose value depends on understanding exponential learning curves, data network effects, or multi-platform convergence dynamics are therefore systematically excluded from the portfolios of most institutional investors, not because those investors have assessed and rejected these positions but because those positions fall outside the analytical vocabulary their institutions use.

Wood’s critique of the discounted cash flow approach to valuing innovative companies is not an argument against rigorous financial analysis; it is an argument for analysis that matches its tools to its subject. DCF analysis is appropriate for companies operating in stable competitive environments where historical cash flows are informative about future cash flows. It is not appropriate for companies in which the relevant competitive dynamics are exponential, the asset base is primarily in data and learning systems rather than physical capital, and the total addressable market is actively created by the company’s own operations rather than pre-existing demand. Applying DCF to Tesla or to the early Amazon Web Services is not conservative; it systematically underestimates value in ways that create persistent mispricing.

The case of Nvidia illustrates a different dimension of Wood’s analytical approach. She acknowledges Nvidia’s centrality to the current AI infrastructure build-out—its GPUs are the primary computing substrate for training large-scale neural networks—while arguing that its valuation already reflects, and may exceed, the economic value it will capture from this position. This is not a bet against Nvidia’s technology; it is a recognition that the period of maximal scarcity for AI compute — the period that most benefits Nvidia — may be shorter than consensus expects. As alternative chip architectures mature and software optimization reduces compute intensity per unit of AI capability, the pricing power that currently supports Nvidia’s margins may be compressed. More importantly, from a portfolio construction standpoint, Nvidia is an infrastructure provider: it captures a share of AI developers’ spending but does not itself accumulate the proprietary data and learning systems that Wood identifies as the durable source of AI-era value.

Palantir’s inclusion in Wood’s framework is analytically interesting because Palantir is structurally unlike any other publicly traded company. It was built from the ground up to solve one of the hardest problems in applied data science: how to make AI tools accessible to organizations — governments, militaries, and large corporations — that have enormous amounts of proprietary data but lack the internal capability to build bespoke AI systems. Palantir’s approach is to embed its engineers inside client organizations for extended periods, building tailored AI infrastructure that integrates with existing data systems rather than replacing them. The result is that Palantir’s value to clients compounds over time — each integration makes Palantir’s platforms more deeply embedded and harder to displace. Wood sees this compounding relationship as a structural moat that will allow Palantir to capture a disproportionate share of large institutions’ AI transformation spending globally.

Dollar-cost averaging—the practice of investing fixed amounts at regular intervals regardless of price — is Wood’s recommended approach for retail investors engaging with innovative companies, and it is worth examining why. In conventional investing, dollar-cost averaging is primarily a behavioral tool: it prevents investors from making large commitments at market peaks by automating the investment process. In Wood’s framework, it serves a different purpose. Because innovative companies exhibit higher short-term volatility than the market as a whole, any single investment point may coincide with a temporary peak driven by sentiment rather than fundamental value. Regular investment over time averages out volatility and aligns the investor’s cost basis with the long-term value trajectory rather than with any particular sentiment cycle. The implicit condition is that the investor must have genuine conviction in the long-term direction, not because markets are unpredictable in the short run, but because conviction is what makes it possible to continue investing through the inevitable periods of drawdown.

The concept of paradigm risk — the risk of operating with the wrong model — is Wood’s most important contribution to investment theory and the one most systematically ignored by mainstream finance. Standard risk frameworks treat investment risk as the probability-weighted distribution of returns around an expected value. This is appropriate when the distribution of outcomes is stable and can be estimated from historical data. It is not appropriate when the fundamental structure of the economic environment is changing — when the distribution of outcomes is itself shifting. In such environments, the greatest risk is not making a bad bet within a stable framework; it is making all your bets within a framework that turns out to be wrong. Wood is arguing, in effect, that the greatest risk facing institutional investors today is not volatility within their current models but the obsolescence of those models themselves.

The temporal dimension of Wood’s investment philosophy — her insistence that the relevant horizon is five to ten years rather than one to three — is not arbitrary. It reflects a specific claim about how exponential systems develop. In the early phases of exponential growth, the trajectory looks disappointingly linear: the numbers are small, the progress is incremental, and the timeline to significant impact keeps being pushed out. Investors who evaluate emerging technologies against their current performance rather than their rate of improvement will consistently exit too early — will sell in the phase when exponential growth is just beginning to become visible to non-specialists. Wood’s five-to-ten-year horizon is designed to capture the exponential growth phase that immediately follows this early linear-looking phase — the phase when the compounding effects first become large enough to dominate other economic signals.

The faith element Wood introduces at the end of her investment framework — the claim that buying shares in innovative companies is “investing in a better future” — is easy to dismiss as motivational language. But it describes something real about the psychology of long-term innovation investing that purely quantitative frameworks miss. The investors who held positions in Amazon through its multiple 50-plus percent drawdowns between 2000 and 2015 or who held Tesla through its near-bankruptcy in 2008 and its subsequent volatility could not have maintained those positions purely on the basis of quantitative models — because the quantitative models, at several points, correctly suggested that the downside risk was very real. What sustained them was a structural belief about the direction of economic development — a belief that the problems these companies were solving were real, important, and soluble, and that the companies themselves were the best available instruments for solving them. This is not the same as blind faith; it is a conviction grounded in analysis with a longer time horizon than consensus. Wood’s achievement is making this conviction intellectually respectable rather than merely temperamental.

Economic Projections and Global Growth

ARK Invest’s projection that the convergence of its five key platforms could push real global GDP growth above 7 percent annually over a five-year horizon is, by the standards of mainstream macroeconomic forecasting, extraordinary. The long-run average for global real GDP growth since 1960 is approximately 3.5 percent per year; the post-2008 average in advanced economies has been closer to 2 percent. To project a doubling of the historical long-run growth rate requires a theory of why this time is structurally different — not just cyclically better — and Wood has one. Understanding whether that theory is credible requires examining it against both the historical record of previous general-purpose technology transitions and the specific characteristics of the current one.

The closest historical precedent for what Wood is describing is the electrification of industrial economies between approximately 1890 and 1930. During this period, the adoption of electric motors across manufacturing transformed productivity in ways not previously observed in existing economic data. Paul David’s celebrated analysis of this transition showed that the full productivity benefits of electrification did not appear in aggregate economic statistics for several decades after electric motors became widely available because realizing those benefits required reorganizing entire factory-floor layouts and management practices — organizational changes that could not occur instantly. This insight — the productivity paradox — has been deployed repeatedly to cast doubt on the economic impact of digital technologies, including AI. Wood’s implicit response to this objection is that AI, unlike previous general-purpose technologies, does not require the same degree of organizational redesign because it can be embedded in existing workflows through software rather than requiring changes to physical infrastructure.

The macroeconomic mechanism through which the five-platform convergence generates exceptional growth is best understood as a simultaneous shift in both the production frontier and the adoption rate. Normally, technological innovation shifts the production frontier — it makes previously impossible things possible — but adoption is slow because it requires capital investment, skill development, and organizational change. What is distinctive about the current wave is that AI dramatically reduces the cost and time required for adoption by automating the translation of new capabilities into operational deployment. This means that the gap between frontier innovation and average productivity — historically measured in decades — may compress to years or even months. If this compression is real, it would explain both the anomalously high growth projections and the difficulty of seeing the effect in current aggregate data.

Wood’s argument about the transformation of what constitutes “capital” is perhaps the most consequential macroeconomic claim she makes. Standard growth accounting — the framework used by most economists to decompose GDP growth into contributions from capital, labor, and total factor productivity — defines capital as physical productive assets: machinery, buildings, infrastructure. Intellectual property is treated as a partial exception, but the broader category of data — the trained neural networks, the proprietary datasets, the algorithmic systems that increasingly constitute the core productive assets of AI-era companies — has no adequate representation in standard capital accounting. This means that national accounts systematically undercount investment in the most economically important assets of the current period. If the ratio of real investment to measured investment is large and growing, the gap between measured and actual productivity growth may be substantial.

The geopolitical implications of this economic transformation are among the most politically consequential and least analytically developed dimensions of Wood’s framework. Her claim that nations that understand data will control the future gestures toward what might be called a theory of informational comparative advantage. In the industrial era, natural resource endowments — coal, iron ore, agricultural land — determined much of the pattern of international economic advantage. In the digital era, the relevant endowments are data infrastructure, human capital in quantitative disciplines, and institutional capacity for rapid technological adoption. These are distributed very differently across the world than physical resources, and they are, in principle, more susceptible to intentional development through policy. A nation that invests heavily in mathematics education, research infrastructure, and regulatory frameworks that enable AI deployment can close the gap with established economic powers in a generation — a timeline that has no precedent in the history of industrial development.

The distributional consequences of the growth Wood projects are real and require more careful analysis than her framework typically provides. Historical experience with general-purpose technology transitions shows that aggregate growth typically coexists with, and in the short run may be caused by, significant sectoral disruption and labor market displacement. The electrification transition destroyed millions of jobs in horse-related industries, candle manufacturing, and certain categories of craft production while creating more jobs overall. The digital revolution eliminated routine cognitive work while creating new forms of high-skill knowledge work. AI-driven automation will displace jobs in ways that are already visible — in logistics, customer service, financial analysis, legal research — while creating new forms of work whose contours are not yet clear. The net employment effect is likely positive in the long run, but “the long run” is not a politically adequate timescale for populations facing short-run displacement.

The relationship between economic growth and crisis that Wood identifies is grounded in a genuine historical regularity: many of the most consequential technological innovations of the past two centuries were developed or deployed in response to crises that disrupted existing supply chains, made conventional approaches unworkable, or created political conditions favorable to rapid change. The First World War accelerated the adoption of aviation and chemical production; the Second World War drove advances in computing, radar, and nuclear physics; the oil shocks of the 1970s spurred the development of the modern solar energy industry. Wood’s claim that the current period of geopolitical and economic uncertainty may accelerate rather than retard the adoption of innovation is not wishful thinking; it reflects a structural feature of how technological transitions actually occur under competitive pressure.

The most profound macroeconomic implication of Wood’s framework is the one she states most directly and mainstream economists take least seriously: that the economic categories through which we currently understand wealth, growth, and development are inadequate for the economy that AI is creating. An economy in which a significant fraction of productive capacity consists of trained neural networks running on commodity hardware produces wealth through mechanisms that standard capital theory cannot properly account for. The marginal cost of scaling an AI system approaches zero; the intellectual labor required to create it cannot be replicated; the competitive advantage it creates is durable in ways that physical capital is not. These properties — near-zero marginal cost of reproduction, non-rival consumption, compounding returns to scale — describe not the economy of industrial-era goods and services but the economy of knowledge and information. Wood’s broader claim is that AI is transforming an increasing share of previously rivalrous, positive-marginal-cost economic activity into effectively non-rivalrous, near-zero-marginal-cost activity. If this is true, the implications for everything from tax policy to antitrust to international trade law are radical and largely unworked out.

Obstacles, Risks, and the Limits of Optimism

Wood is a better analyst than her critics typically credit because she is a genuine analyst — she engages with risks and limitations rather than simply ignoring them. But she is also a more limited analyst than her admirers typically acknowledge because she is also an asset manager with a commercial interest in the success of the companies in her funds, and this interest shapes which risks she examines closely and which she treats more cursorily. Reading her public commentary on risk requires holding both of these observations simultaneously: she is genuinely thoughtful about systemic risks, but less thorough about company-specific and fund-management risks that are more directly relevant to her own investors’ experience.

The regulatory lag problem Wood identifies — the gap between the pace of technological change and the pace of institutional adaptation — is real and structurally serious. It arises from a basic asymmetry: regulatory frameworks are designed by institutions that remain stable for decades, using legal categories developed for existing economic structures, and through political processes that favor incumbent interests. Technological disruption creates new economic structures faster than these processes can generate updated frameworks. The result is not simply that good technologies are delayed; it is that the regulatory environment becomes increasingly incoherent — a patchwork of rules designed for a world that no longer exists, applied inconsistently to technologies whose fundamental nature those rules were not designed to address. This incoherence creates unpredictable compliance costs, differential barriers to entry for established and new players, and strategic uncertainty that affects capital allocation.

The concentration risk that Wood raises — the possibility that AI-era value creation becomes concentrated in a small number of companies and nations — is, paradoxically, one of the risks most directly created by the convergence thesis she champions. If data is the primary productive asset of the AI era, and if data advantages compound through the flywheel dynamic Wood describes for Tesla, then the economic logic of AI development tends strongly toward concentration. Companies with larger datasets train better models; better models attract more users; more users generate more data. This dynamic has already produced significant concentration in the general-purpose AI model market — a small number of large-scale models trained by a handful of organizations dominate AI capabilities globally. Wood’s response — that AI will democratize access to intelligence in ways that ultimately benefit everyone — is plausible but requires institutional conditions (competitive model markets, open access to basic AI infrastructure, regulatory constraints on data monopoly) that do not currently fully exist.

Wood’s track record demands honest examination in any serious assessment of her framework. ARK Innovation ETF delivered extraordinary returns between 2014 and 2020, significantly outperforming broad market indices. It then delivered equally extraordinary underperformance between 2021 and 2022, losing approximately 75 percent of its peak value — a drawdown that many of its investors experienced more fully than its run-up because assets under management were highest at the peak. The conventional interpretation of this trajectory is that Wood’s concentrated, high-multiple strategy was primarily a beneficiary of the zero-interest-rate environment of the 2010s rather than a validation of her investment thesis. As rates rose and the discount rate applied to long-duration growth assets increased, the valuations generated by Wood’s framework became unsustainable. This interpretation is partially correct but also incomplete: the drawdown reflected both valuation compression and genuine company-specific disappointments in several holdings, and the subsequent partial recovery reflected both the return of growth sentiment and genuine improvement in some underlying businesses.

The volatility problem is not merely a feature of Wood’s strategy; it is a structural characteristic of investing at the frontier of technological change that no strategy adjustment can fully address. Companies operating at the convergence of emerging platforms face genuine uncertainty about which specific implementations will win, regulatory timelines, the pace of technological improvement, and competitive dynamics that shift as more capital enters the space. This uncertainty is real, not illusory — it cannot be managed away through better analysis because it is a fundamental property of systems that have not yet reached stable competitive equilibria. Volatility in high-innovation portfolios is therefore not a signal that the underlying thesis is wrong; it is a signal that the thesis is engaging with systems whose outcomes are genuinely undetermined. The investor’s question is not how to eliminate this uncertainty but how to take positions on it in ways that reflect its true character.

The bioethical dimensions of multi-omics biotechnology are the place in Wood’s framework where the argument most clearly outpaces its ethical infrastructure. The ability to sequence individual genomes at a population scale, to predict disease with high accuracy years before clinical onset, and to intervene in gene expression in somatic or germline cells creates capabilities whose implications for medical ethics, insurance markets, privacy rights, and human identity are profound and contested. Wood engages with these questions at the level of acknowledging that “ethical wisdom must accompany scientific progress” — which is true but insufficient. What is specifically at stake—questions about genetic privacy in insurance contexts, about access to expensive genomic therapies, about the ethics of germline editing in human embryos — requires more detailed engagement than a general admonition to be wise. This is not a criticism specific to Wood; it is a criticism of how the investment community broadly engages with the bioethical dimensions of the technologies it funds.

The education and institutional alignment problem Wood identifies may be the most practically consequential barrier to the economic transition she describes. An economy organized around AI-era productive assets requires a workforce with mathematical literacy, computational thinking, and the capacity for continuous learning — skills that are developed over years and decades and cannot be conjured by labor market demand alone. Current educational systems in most of the world remain organized around the knowledge and skill demands of the industrial era: standardized curricula, batch processing of students through fixed grade levels, terminal certification rather than continuous development. The gap between what the AI economy requires of its participants and what educational institutions currently produce is growing faster than those institutions are reforming. Wood acknowledges this gap but does not fully engage with the political economy of why it persists and what would be required to close it.

Holding Wood’s optimism and these criticisms simultaneously produces a view that is more nuanced and more defensible than either pure optimism or pure skepticism. The fundamental technological thesis — that AI, energy, robotics, blockchain, and multi-omics are converging in ways that will generate significant economic value — is well-grounded. The claim that this convergence will produce smooth and broadly distributed economic growth, that regulatory environments will adapt at the required pace, that concentration risks will be mitigated by competitive market forces, and that the ethical challenges of these technologies will be resolved by a combination of scientific conscience and institutional wisdom — these claims require considerably more skepticism. What Wood is right about is the direction and approximate magnitude of the technological transition. What requires more careful examination is the distribution of its benefits and costs — a question whose answer depends as much on political will and institutional design as on the underlying technology.

Implications for Investors and a Strategic Synthesis

The most important implication of Wood’s framework for serious investors is not a specific position recommendation but a methodological one: the need to develop analytical capabilities appropriate to the current environment rather than inherited from the previous one. This is harder than it sounds. Investment institutions are built around processes designed to produce defensible, replicable analyses of companies in stable competitive environments. The analysts they hire are trained in these methods; the risk frameworks they use are calibrated to historical volatility patterns; the incentive structures they operate under reward consistency with peers. Developing genuine competency in evaluating exponential technology platforms requires organizational change — changes in hiring, in analytical methodology, in risk management, and in stakeholder communication — that most institutional investors have barely begun.

The paradigm shift in portfolio construction that Wood’s framework implies moves away from sector allocation — the convention of dividing a portfolio into percentages of industrial exposure across energy, healthcare, technology, financials, and so on — toward what might be called “platform allocation”: exposure to the specific technological platforms and their convergence zones that will define economic structure over the next decade. The practical difference is significant. A sector allocation approach might allocate 15 percent of a portfolio to “technology” — a category that includes both legacy software businesses and genuinely AI-native platforms — treating them as a single, coherent exposure. A platform allocation approach would distinguish between these by overweighting companies building real-world AI systems and underweighting companies that sell software to organizations still operating on industrial-era logic.

Dynamic diversification — Wood’s term for maintaining exposure across the full range of converging innovation platforms rather than concentrating on the apparent leader at any given moment — serves two distinct analytical functions. The first is risk management: by maintaining exposure across five platforms rather than one or two, the portfolio is protected against a scenario in which a specific platform’s development is delayed by technical or regulatory setbacks. The second function is opportunity capture: because the value of convergence resides at the intersections of platforms, an investor who holds only AI-related companies but not energy storage companies misses the full value created by the integration of autonomous vehicles and grid-scale renewable energy. The diversification is not across independent risks but across correlated opportunities — a subtly but importantly different analytical basis.

The moral dimension of investment choice that Wood articulates is genuinely important for a class of investors — sovereign wealth funds, university endowments, pension funds, family offices with multi-generational time horizons — whose decisions carry implications beyond the financial returns of any single fund or generation. These institutions are not simply maximizing risk-adjusted returns; they are allocating the productive capital of societies, institutions, and families over decades. For such investors, the choice of what to fund is inseparable from the choice of what kind of economy to bring into existence. Wood argues that investors in this category face a genuine moral obligation to engage with this dimension of their decisions — not because it changes the financial calculus, but because the financial calculus, properly understood over the relevant time horizon, already incorporates it. Long-term economic returns and the health of the civilizational infrastructure that generates them are inseparable.

The implications for Asia — and for Indonesia specifically — are among the most practically important dimensions of Wood’s framework for the readers most likely to engage with this essay. Wood’s claim that “nations that understand data will dominate the future” is not a metaphor; it describes a specific competitive dynamic in which national investments in data infrastructure, technical education, and AI-enabling regulation translate into economic advantage at a speed without precedent in the history of industrial development. Indonesia, with a population of 280 million people, a rapidly growing digital economy, and a geographic position at the center of maritime Southeast Asia’s trade flows, has structural assets that Wood’s framework would identify as relevant. But structural assets are not competitive outcomes. The gap between possessing relevant raw materials — young population, large data generation, and strategic geography—and developing the institutional capacity to translate them into AI-era economic leadership is substantial and will not close without deliberate policy choices.

The transformation of global economic leadership that Wood’s framework implies is not a smooth handover from existing powers to new ones. It is a disruption that will be resisted by incumbents — nations, corporations, and institutions that have built their current positions around the rules and assumptions of the industrial era. The political economy of this resistance is already visible: regulatory frameworks that favor established industries over disruptive entrants, trade policies that restrict cross-border data flows in ways that disadvantage AI development in smaller markets, and educational systems that certify skills for jobs that are being automated. Understanding Wood’s framework fully requires understanding not just the technological trajectory she describes, but also the political and institutional forces that will shape how that trajectory unfolds in different national contexts.

The concept of investment as civilization-building rather than mere capital allocation takes its most concrete, least rhetorical form when applied to specific institutional choices. A pension fund that diverts capital from fossil fuel companies to energy storage and renewable energy infrastructure is not just making a bet on the energy transition; it is providing the patient capital that makes the infrastructure build-out economically viable at the required scale and speed. A university endowment that invests in genomic medicine research and the companies commercializing it is not just generating returns; it is funding the development of medical capabilities that will reduce suffering at a scale that public health systems cannot. These are not incidental effects of investment choices made on financial grounds; they are direct outcomes of decisions about where capital flows. Wood’s insistence that investors recognize this agency is not sentimentality — it is accuracy.

The strategic synthesis that follows from Wood’s framework is this: the next decade will reward investors who can distinguish between companies native to the AI-era economy and those adapting industrial-era business models to survive the AI transition. This distinction is harder to make than it appears because the surface characteristics of these two categories often look similar — both types of companies use AI, both generate significant data, both hire machine learning engineers. The difference lies in whether AI is core to the company’s competitive architecture or peripheral to it; whether data is a structural moat or an operational input; whether the company’s economics improve as AI capabilities advance or remain roughly constant. Wood’s analytical achievement is developing a framework for making this distinction systematically, and her deepest challenge to the investment community is to build the analytical capacity required to apply it rigorously.

Conclusion

The intellectual significance of Cathie Wood’s framework extends well beyond the specific investment positions it generates. She is arguing, at its deepest level, that the current technological transition is of the kind that occurs only a few times per century — a transition that changes not just what can be produced but how economic value is created, measured, and distributed. This kind of argument demands engagement at its deepest level: not with the specific stock picks or the five-year price targets but with the underlying theory of how technological revolutions unfold and what they require of the institutions, individuals, and societies that experience them.

The transition from linear to exponential economic logic that Wood describes is not simply a feature of specific technologies. It is a change in the fundamental dynamic of competitive advantage. In linear environments, competitive advantages erode slowly and can be defended through incremental improvement. In exponential environments, competitive advantages can be built at extraordinary speed by early movers — and can be lost equally quickly by incumbents who fail to recognize that their existing advantages do not transfer to the new environment. The historical examples of companies and even entire industries that failed to survive general-purpose technology transitions — the railroad companies that should have been early airlines, the film photography companies that should have built digital cameras — are cautionary tales not of incompetence but of genuine difficulty in recognizing when an environmental shift is fundamental rather than incremental.

The moral framework that Wood wraps around her economic argument is not optional decoration. It is integral to understanding why she makes the specific analytical choices she does — why she chooses long time horizons over short ones, why she accepts high volatility rather than seeking to minimize it, why she maintains conviction through periods of significant drawdown. These choices cannot be made consistently on purely quantitative grounds; they require a stable set of commitments about what economic activity is for and what constitutes genuine value creation over the relevant human timescale. Wood’s answer — that genuine value creation is the expansion of human capability and the reduction of preventable suffering — is a specific philosophical position that can be argued with, but cannot be dismissed as irrelevant to investment decision-making.

The synthesis of empirical rigor and moral commitment that Wood attempts is rare in public financial discourse and is worth taking seriously on its own terms. Most public investment commentary either pretends to be purely empirical — all data, no values — or is openly value-driven in ways that are indifferent to empirical evidence. Wood’s attempt to hold both together, to ground her moral commitments about the direction of human development in empirical analysis of technological trajectories, is genuinely difficult to sustain and is, frankly, imperfectly executed. Her empirical analysis is stronger in some areas than others; her moral reasoning occasionally lapses into the kind of unexamined progressivism that treats technological advance as self-evidently good rather than contingently beneficial depending on how its fruits are distributed. But the attempt itself — to integrate empirical and normative reasoning in investment analysis — is correct and important.

For the intellectual and professional communities that engage most seriously with questions of economic development and technological change — academic economists, policy architects, institutional investors, technology analysts — Wood’s framework poses several specific challenges. For economists: the challenge of developing macroeconomic frameworks adequate to AI-era capital, in which the most important productive assets are learned systems rather than physical machines. For policy architects: the challenge of designing regulatory environments that allow genuine technological innovation to proceed at its natural pace while preventing the concentration risks and ethical failures that unregulated technological development produces. For institutional investors: the challenge of building analytical and organizational capacity adequate to the task of evaluating convergent technology platforms. For technology analysts: the challenge of maintaining honest engagement with both the possibilities and the limitations of the technologies being analyzed, rather than cycling between uncritical boosterism and reflexive skepticism.

The Southeast Asian context — and Indonesia’s place within it — frames these challenges in terms that are both globally general and locally specific. The global dynamic Wood describes will play out differently in different national contexts depending on the quality of digital infrastructure, the depth of technical education, the sophistication of regulatory environments, and the capacity of local capital markets to provide patient, long-horizon investment. Indonesia’s current position in this landscape is one of significant potential and significant underdevelopment: the potential derived from scale, youth demographics, and digital adoption rates; the underdevelopment derived from infrastructure gaps, regulatory uncertainty in technology sectors, and educational systems that have not yet fully oriented themselves toward the skill demands of an AI-era economy. Translating Wood’s global framework into locally actionable insight requires exactly the kind of contextual specificity that the framework itself, being necessarily general, cannot provide.

The epistemological lesson that cuts across all of Wood’s specific claims is this: the most dangerous form of ignorance in a period of rapid technological change is not the ignorance of specific facts but the ignorance of paradigm — the failure to recognize that the framework through which you are interpreting facts has become inadequate to the facts themselves. This is the hardest form of ignorance to correct because it is self-concealing: within a paradigm, everything looks coherent, the anomalies are manageable, and the framework seems to work well enough. It is only when the accumulation of anomalies becomes overwhelming that the inadequacy of the framework becomes undeniable — and by then, the cost of the delay is substantial. Wood’s contribution, at its best, is to create conditions in which paradigm inadequacy becomes visible earlier than it would otherwise. This is a valuable intellectual service regardless of whether any specific prediction she makes proves correct.

The Big Shift, ultimately, is a claim not just about economic trajectories but about the relationship between knowledge and power in the twenty-first century. The industrial era was organized around the control of physical resources and physical production; the capacity to extract, process, and move physical matter was the primary determinant of economic and political power. The era Wood describes will be organized around the control of cognitive resources — the capacity to accumulate, process, and generate knowledge — and this reorganization will be as consequential for political power as for economic outcomes. Nations, institutions, and individuals that understand this transition early and invest accordingly will not just achieve superior financial returns; they will participate in shaping the institutional architecture of the new era. Those who understand it late will adapt to an architecture they did not design and do not control.

For intellectuals, the appropriate response to Wood’s framework is neither adoption nor dismissal but rigorous engagement. The strongest elements of her argument — the convergence thesis, the paradigm critique, the theory of compounding data advantages, and the macroeconomic case for a step-change in productivity — deserve sustained analytical engagement that goes further than the podcast format can accommodate. The weaker elements — the distributional assumptions, the regulatory optimism, the ethical underdevelopment of the biotech argument — need exactly the critical examination that independent intellectual communities are positioned to provide. The value of an intellectual tradition is not in its capacity to generate comfortable consensus but in its capacity to engage hard questions without predetermined outcomes. The questions Wood is raising are among the hardest and most consequential of our time. They deserve the most serious treatment we can bring to them.

This essay is an intellectual analysis of the investment and philosophical framework articulated by Cathie Wood, drawing on her public statements and ARK Invest’s research. It does not constitute financial advice. All investment decisions carry risk, and readers should conduct their own analysis and seek qualified professional guidance before making investment decisions.

About The Author

Artikel Terkait

Artificial Intelligence and the World Order of 2040: A Strategic Essay on AI, Extraterrestrial Intelligence, and the Future of Humanity

Artificial Intelligence and the World Order of 2040: A Strategic Essay on AI, Extraterrestrial Intelligence, and the Future of Humanity

The Six Epochs of Intelligence: Ray Kurzweil, AI, and the Cosmic Future of Mind

The Six Epochs of Intelligence: Ray Kurzweil, AI, and the Cosmic Future of Mind

Acehnology: Menyelami Kembali Kosmos Pengetahuan dari Tanah Aceh

Acehnology: Menyelami Kembali Kosmos Pengetahuan dari Tanah Aceh

Cryptocurrency and Human Behavior in Cyberspace: Trust, Risk, and Digital Tokens

Cryptocurrency and Human Behavior in Cyberspace: Trust, Risk, and Digital Tokens

Planetary Civilization: Ketika Teknologi, Informasi, dan Algoritma Membentuk Masa Depan Manusia

Planetary Civilization: Ketika Teknologi, Informasi, dan Algoritma Membentuk Masa Depan Manusia